Why is a Credit Score Important?

Why is a Credit Score Important?

In today’s tough economic times, where every person is being

evaluated by a number (Credit Score), having a good Credit Score is

an essential to enjoy an appropriate standard of living. You need to

have a good credit just to rent an apartment, rent a car, open a

bank account, get insurance, get a job, buy a car or obtain a home

mortgage. Depending on your Credit you will be denied, will be

offered a good rate, or will be offered with higher than normal

rate/down payment, etc.

Like most cases in finance, those with the lowest risks get to pay

the lowest rates.

To mortgage lenders, your credit score represents your likelihood of

making on-time mortgage payments for the next couple of years.

Therefore, it is very important to have a good/excellent credit

history and credit score. You also need to know what is in your

credit reports and what your credit score is.

Credit scores play a major role in determining for which mortgage

product or loan you will qualify, and to which rate you will be

assigned by your lender.

In April 2008, both Fannie Mae and Freddie Mac introduced something

called Loan-Level Pricing Adjustments (LLPAs),

also known as “Loan Delivery Fees”.

Loan-level pricing adjustments are percentage of a loan

amount added to a loan fee, based on a specific borrower’s FICO

credit score and LTV.

Table 1 shows these LLPA adjustment based on the LTV and Credit

Score:

|

Table 1: LLPA by Credit Score/LTV |

|

|

LLPAs by LTV Range |

|

<=60.00% |

60.01-70.00% |

70.01-75.00% |

75.01-80.00% |

80.01-85.00% |

85.01-90.00% |

90.01-95.00% |

95.01-97.00% |

97.01-100% |

|

Credit Score |

|

|

>= 740 |

-0.250% |

0.000% |

0.000% |

0.250% |

0.250% |

0.250% |

0.250% |

0.250% |

N/A |

|

720 – 739 |

-0.250% |

0.000% |

0.250% |

0.500% |

0.500% |

0.500% |

0.500% |

0.500% |

N/A |

|

700 – 719 |

-0.250% |

0.500% |

0.750% |

1.000% |

1.000% |

1.000% |

1.000% |

1.000% |

N/A |

|

680 – 699 |

0.000% |

0.500% |

1.250% |

1.750% |

1.500% |

1.250% |

1.250% |

1.000% |

N/A |

|

660 – 679 |

0.000% |

1.000% |

2.000% |

2.500% |

2.750% |

2.250% |

2.250% |

1.750% |

N/A |

|

640 – 659 |

0.500% |

1.250% |

2.500% |

3.000% |

3.250% |

2.750% |

2.750% |

2.250% |

N/A |

|

620 – 639 |

0.500% |

1.500% |

3.000% |

3.000% |

3.250% |

3.250% |

3.250% |

3.000% |

N/A |

|

< 620 |

0.500% |

1.500% |

3.000% |

3.000% |

3.250% |

3.250% |

3.250% |

3.250% |

N/A |

Source:

https://www.fanniemae.com/content/pricing/llpa-matrix.pdf

Published 9/20/2012

Note: For loans with LTV > 80%, additional fee known as PMI (Premium

Mortgage Insurance) will be added to the Mortgage payment.

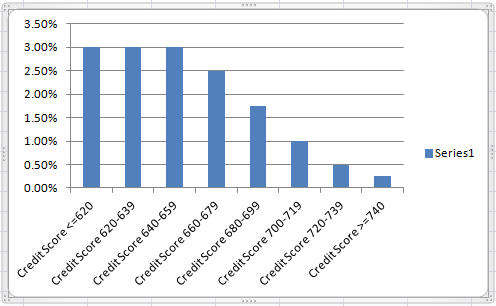

Table 2: Affect of FICO Credit Score on

Loan-Level Pricing Adjustment Percentage of the Loan Amount

Assuming 20% down (LTV =80%)

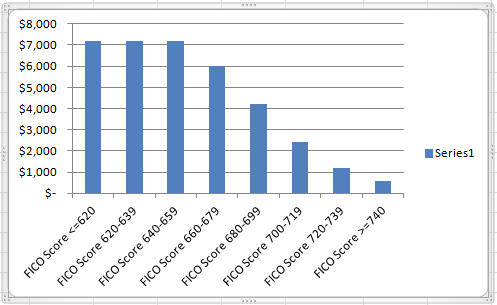

Table 3: Affect of FICO Credit Score on

Loan-Level Pricing Adjustment Added Fee

Assuming Purchase Price of $300,000 and 20% down (LTV =80%)

For a given LTV (Loan-To-Value):

·

The higher your credit score, the lower your

Loan-Level Pricing Adjustments (LLPA)

rate will be.

·

The higher your credit score, the lower your LLPA Added Fee +

Mortgage Insurance will be.

·

The higher your credit score, the lower your mortgage or interest

rate will be.

·

Example 1:

A home purchase at $300,000 with 20% down carries a Mortgage loan of

$240,000. LLPA added loan fees which are due at closing for borrows

with credit score of 741 and 655 are $600 and $7,200, respectively.

As you see, the borrower with lower credit score of 655 will pay

extra amount of

$6,600

compare to the borrower with credit score of 741. This shows an

example of a negative impact or cost of a low credit score on a

mortgage loan.

Example 2:

the monthly payment (Principal + Interest) of a $250,000 loan with

30-year fixed rate of 3.5% and 4.5% would be $1266.71 and 1122.61,

respectively. 1% increase in the interest rate in our example will

cost the borrower an additional $51,876 in his/her 30-year loan

term.

Conclusion:

Credit scores play a major role in determining for which mortgage

product or loan you will qualify, and to which rate you will be

assigned by your lender.

The higher your credit score, the lower your mortgage or interest

rate will be.

If you plan to use a mortgage for your next home purchase or buy a

car, you will want to keep your credit scores as high as possible.

Click

What is a Credit Score to see how you can access to your credit

score.

Click this link to see

What makes up a credit score and tips on how to improve it.

By the Way, time is 11:00 AM, do you know what your credit score is?

|