|

What

is an Adjustable Rate Mortgage (ARM) and who can benefit from it?

Adjustable Rate Mortgages (ARM)

1-Year

ARM, Caps of 2/6? 1-Year

ARM, Caps of 2/6?

An Adjustable Rate Mortgage is a mortgage loan in which

·

The interest rate adjusts periodically according to a predetermined index and

margin.

·

The adjustment of the interest rate results in the mortgage payment either

increasing or decreasing.

·

Periodic adjustments to the interest rate can occur every six months, every year

or in multiple years.

·

ARMs typically have a lower initial interest rate vs. fixed.

·

There are ARMs that have fixed periods for 3, 5, 7 or even 10 years before the

interest rate starts adjusting (Hybrid ARM)

ARM

Terminology

Initial

Rate

The rate at which an ARM program begins is called the initial rate. The initial

rate and payment amount on an ARM will remain in effect for a limited period of

time. The initial rate can range from 1 month to 5 years or more.

Adjustment Period

The interest rate and monthly payment change every month, three months, six

months, 1 year, 3 years, 5 years or 7 years or so. The period between rate

changes is called the adjustment period. For example, a loan with an

adjustment period of 1 year is called a “1-year ARM” and the interest

rate and, therefore, payment can change once every year. Remember, the interest

rate’s change could be positive or negative, it means at the next adjustment

period, depending on the market, the interest rate could be higher or lower than

the existing interest rate.

Index

The index is what the lender uses as an instrument for measuring changes in

interest rates. It is the lender’s barometer of change in interest rates.

Increases or decreases in the index cause the ARM payment to increase or

decrease accordingly.

Prevailing indexes include:

• 1 Year Constant Maturity Treasury Rate (CMT)

• 11th District Cost of Funds Index – COFI.

It is also known as San Francisco 11th District Cost of Funds Index

– COFI.

This

is

often used as an index for adjustable-rate mortgages

• London Interbank Offered Rate - LIBOR

Margin

The percent added to the index in order to calculate the payment interest rate.

The Margin is the profit the lender will make above the index. The margin never

changes during the life of the ARM.

Fully Indexed Rate

The fully indexed rate is equal to the margin plus the index and is usually to

the nearest one-eighth of a percent. For example, if the lender uses an index

that currently is 1% and adds a 2% margin, the fully indexed rate would be:

Index

=1% +

Margin =2%

=============================

Fully Indexed Rate =3%

Discounted Initial or Indexed Rate (“teaser rate”)

If the initial interest rate on the loan is less than the fully indexed rate, it

is called the discounted initial or indexed rate. A lower interest rate

is offered by the lender during the first year or more of the loan. These

interest rate concessions are used as incentives to attract borrowers to ARM

products.

Interest-rate caps

An interest-rate cap places a limit on the amount the interest rate can increase

or decrease. Rate caps limit how much interest can be charged. Interest caps

come in three types:

Per Adjustment Cap

·

This caps limits how much a payment may increase or decrease in any subsequent

adjustment. In most cases, lenders base the per adjustment cap off the initial

or start rate. No matter what the Index + Margin calculates to at the time of

adjustment, the per adjustment cap applies.

Lifetime Cap

·

This cap is the limit the interest rate increases over the life of the loan.

This is a worst case scenario. The highest the payment will ever go to no matter

what the Index and Margin add up to.

Initial Adjustment

Cap

·

ARM’s that offer a fixed rate period during the first years of the loan usually

have an initial rate cap that is higher than the per adjustment cap. In many

ARM’s the interest payment rate may increase as much as 6% higher than the first

year rate.

ARM Cap Terminology

1/4 ARM

– 1% per adjustment cap and a 4% lifetime cap

2/6 ARM

– 2% per adjustment cap and a 6% lifetime cap

4/2/6 ARM

– 4% initial adjustment cap, 2% per adjustment cap and a 6% lifetime cap

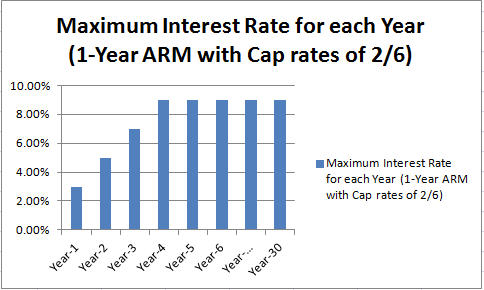

Example: 1-Year ARM, ARM Caps of 2/6. How does the ARM work?

The

11th District Cost of Funds (COFI) is often used as an index for adjustable-rate

mortgages. At the time of writing this article, the

COFI rate was 0.999%. Let’s assume 1%

If the index is 1% and the lender’s margin is 2% on a 1-year ARM, the

fully indexed payment rate would be 3% (1% + 2%) during the first year.

If the caps are 2/6, the most the interest rate could move up after the first

year would be 5% (3% initial rate plus 2% adjustment cap). Depending on what the

index does after the first year, the actual interest rate could in fact be

lower, but the maximum it could adjust upward is 5%.

Also, the maximum the interest rate could move for the entire life of the loan

would be 9% (3% initial rate plus 6% lifetime cap). If the index increased the

maximum every year, the borrower could reach the 9% maximum in the 4th

year (this is the worst case scenario).

Advantages of ARM Loans

1.

Lower initial interest rate:

The initial rate of interest will almost always be considerably lower

than the best fixed rate mortgage deal in the short-term. Please note and

emphasize on the key points here: ARM Initial rate for a short period of time

will be lower than the best fixed rate at the time.

2.

The low initial low ARM

can help borrowers

who are currently struggling, but are confidence to experience income growth

later in their professional career.

3.

Higher Loan Amount:

The low introductory or initial rate allows a home buyer to borrow a larger sum

of money and purchase their dream home because home mortgage payments are

initially considerably lower.

4.

If Rates

Falling:

If the interest rates fall or stay low at the time of

Adjustment

Period, the home buyer benefits financially. The more rates fall down or the

longer they stay low, the more financial benefit to home buyer.

Disadvantages of ARM Loans

1.

More Long Term Cost:

While the initial

interest rates are lower than rates on fixed-rate loans, an ARM mortgage loan

could actually cost the borrower much more over the full duration.

2.

Unpredictable Home Mortgage

Payment:

Unlike the fixed-rate mortgage interest, the rate of interest is not set and

could go up a lot during the loan term. This could make it difficult for those

who are on a fixed income to cope with rising payments when banks rates start to

go up.

Warning: More Foreclosure.

For the above reason, foreclosure rates have always been a lot higher on ARM’s

than fixed-rate deals.

Contact us about your Real Estate

Questions

|